Last day I was talking to the owner of an electronic devices store. He

was explaining how for some of the items he sells, his selling price is

less than his actual purchase price. For imported items (like Toshiba

laptops in this case) the amount he has to pay is in dollars but the

Maximum Retail Price advertised by the company and printed on its

catalog are in rupee. According to him, it takes around 4-5 months for

consignment to arrive at his store, and by the time products are

delivered to him, value of rupee gets devalued and he has to pay at

current exchange rate but his customers will pay him only in printed

MRP.

I did not believe him completely for the difference in amount he told

me was far more than the actual devaluation of rupee in last 6 months.

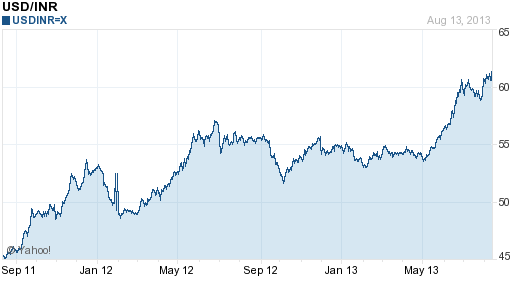

But it is hard to ignore the rapid pace with which rupee is

depreciating. As you can see in the chart, the value of dollar in rupee

has increased from 45 to 61 in last two years. That is around 35%. In

other words, value of rupee has depreciated by 35% (assuming inflation

of dollar to be negligible).

Let us delve into this fascinating (though, painful in this case)

phenomena of macro economics and try to understand its causes, impact

and what our government can do to minimize its ill effects.

Exchange Rate Mechanism

Let us first try to understand how exchange rate is determined? All

economies that interact with international economy can be broadly

classified into three categories on the basis of exchange rate policy of

the country.

1.

Fixed Exchange Rate:

These economies peg the value of their currency with some other

prominent currency like US dollar. This system is simple and provides

stability to the economy (of course, if the economy of the country to

whose currency its currency is pegged is stable). This type of exchange

rate regime is maintained by generally smaller economies like Nepal and

Bhutan (pegged to Indian Rupee) or several African nations. Rational

behind such regime is that in case of small economy – if the exchange

rate is market determined – the sudden influx or outflux of even

relatively small amount of foreign capital will have large impact on

exchange rate and cause instability to its economy. Notable exception is

China which despite being large economy has its currency pegged to US

dollar. But then when it comes to China, its irrational to talk about

rationality

.

2.

Floating (or free) Exchange Rate:

Bigger and developed economies like US, UK, Japan etc generally let

market determine their exchange rate. In such economy exchange rate is

determined by demand and supply of the currency.

For example consider exchange rate of US dollar versus Japanese Yen.

If US wants to import certain item from Japan, it will have to pay the

Japanese company in Japanese yen. This is because in common market of

Japan, dollar will not fetch you anything. But the American company will

not have Yen, so it will purchase Yen from the international currency

market. This will increase the demand of Yen and supply of dollar. Thus

the value of Yen vis a vis dollar will increase. Similarly if Japanese

company is importing something from US, it will increase value of dollar

as compared to Yen.

Export-import, though the major, is not the only source for currency

exchange. Capital flow – Americans investing in Japan and Japanese

investing in USA – is also a significant source of currency exchange.

Another source of currency exchange is remittance – that is the money

sent home by Americans working in Japan and vice versa. Cumulative of

all these exchanges determine the exchange rate. If net requirement of

Dollar by Japanese is more than net Yen required by USA, dollar will

appreciate against Yen. You should also understand that this is

oversimplified for the purpose of illustration. In real world, there

will be multilateral interactions and final exchange rate will be

equilibrium reached by all those interactions.

3.

Hybrid system:

Most mid sized economy like India practices a mix of both these regimes.

It allows for the exchange rate to float in a range which it deems

comfortable. Once the market determined rate tries to breach this range,

central bank (government) intervenes in the currency market and

controls the exchange rate.

How does government control exchange rate?

In fixed or hybrid exchange rate regime where government controls

exchange rate, control is exercised by actively participating in

international currency market through its central bank (Reserve Bank of

India or RBI in our case). Suppose there is huge demand of rupee in

India which is driving the value of rupee. Also, lets assume that RBI is

comfortable only in range of Rs 50 to Rs. 60 per US dollar. This rapid

surge in the demand of rupee (which might be because a. Indian export is

far more than its import, b. foreign investors want to invest in India

and c. large number of Indians earning abroad are remitting their money

back home) is pushing the exchange rate below Rs. 50 per dollar. The RBI

will then step in the market and will offer Rs. 50 for each dollar.

Those buying rupees against dollar will now purchase from RBI since its

offering better rate. Soon other traders will have to arrive at this

rate, if they want to participate. Since RBI has the ability to print

currency notes, it can keep the lower limit of exchange rate fixed at

this value. When demand for rupee is subsided, RBI will step back and

let market determine the exchange rate. In the process, RBI will have

accumulated a pool of dollars; this is called forex reserve or foreign

exchange reserve.

Now let us move to other extreme. Suppose Indian exports have

dwindled, imports are on surge, foreign investors are fleeing Indian

market and remittances are at all time low. Now, every one wants dollar

but there is little supply. This will drive the price of dollar up. Its

about to breach the upper limit of Rs. 60/ USD. RBI will step in again

and will put its dollar reserves on sale at the rate of Rs. 60/ USD.

This will stop the further depreciation of rupee.

As you can see, in order to be able to stop the currency from

appreciating, RBI will have to print money and for preventing its

depreciation it needs a reserve of dollar. This constraint has

interesting implications on the current predicament of RBI in the

context of depreciating rupee.

Effect of exchange rate on Import and Export:

Suppose US company wants to buy Indian textile and suppose on T-Shirt

costs Rs. 120 and exchange rate is Rs. 50/$. So for american company the

cost of T-Shirt is $2.4. Now, if rupee depreciates to Rs. 60/$ the

price of T-shirt becomes $2 only. This will make Indian T-shirt cheaper

to buy and will increase its demand. Companies who were importing from

other nations (may be China or Bangladesh) might shift to India and

Indian exports will increase.

Consider the opposite scenario. Rupee appreciates to Rs. 40/$ making

the cost of one T-shirt $3. This will repel US importers and might drive

them to other rival exporters whose garments are cheaper. Thus,

depreciating currency helps exports while appreciating currency has

opposite effect.

Similarly if India imports $ 1000 iPad from US, at exchange rate of

Rs. 60, it will cost Rs. 60000. If currency appreciates to Rs. 50/$ the

price will reduce by Rs. 10000. This might encourage many new people to

by iPad which earlier thought it to be too expensive. Thus, the demand

for imported products will increase in appreciating currency and will

drive imports upward. Depreciating currency will have opposite effect.

Balance of Payment (BoP) Accounts

International monetary transactions of a nation is recorded in two accounts.

1.

Current Account: This

records all the trades (export-import), remittances, interests and

earnings on investments made into out side countries and other flows

which is current in nature (meaning with no intention of future return).

If total inflows in the country (its export, remittances and earning

from its investments abroad) is more than its outflows (its import,

remittances out of the country, payments of interests etc.) then the

country is said to have current account surplus. China, owing to its

huge exports, is currently the nation with largest current account

surplus. Similarly, if outflows exceeds inflows, the country is said to

be in current account deficit. USA has the largest current account

deficit. India too has huge current account deficit (about 120 billion

USD in FY 2012)

2.

Capital Account:

This records all the flow (into or out of the country) made for future

return – investment in stocks, bond or companies, in real estate or FDI

(investment made for setting up of business or industry). It also

includes loans taken from abroad (which actually is investment by

foreign lender into the nation). Foreign Currency Reserves are also part

of Capital account but are generally not reported. A country is said to

be in Capital account surplus if total inflows into the country (FII,

FDI and borrowing from foreign companies/banks) exceeds total outflows

(investments into foreign countries and lending to foreign countries or

companies). In case situation is reversed, country has capital account

deficit.

Payments always get balanced:

You can spend only as much money as you have. Or in other words, total

amount you spend and invest must always be equal to the money you have

earned and loans you have taken. What this means in the context of BoP

is that current account surplus must always be balanced by Capital

account deficit and if a country is having current account deficit, it

must always get equivalent money form of capital account surplus.

BoP and Forex Reserves:

Countries having floating exchange rate and free capital flows do not

have to build foreign currency reserves. But as we have seen earlier,

those who exercise some or full control over exchange rate, do so by

manipulating their Forex Reserves. The difference in current account

surplus and capital account (excluding forex reserves) deficit is

balanced by equal increase in forex reserves (China) and if country is

not able to meet current account deficit by capital flows, then it will

have to liquidate its forex reserve (current situation of India).

For example, China which has huge exports (current account surplus)

as well has huge inflows in FDI and FII, balances this by building up

huge forex reserves as well as by investing in foreign countries.

Chinese government parks large percentage of its surplus into US

government bonds and encourages its government backed and other

companies to buy assets in foreign countries (mostly US). So it

deliberately runs huge capital account deficit so that it can export.

Otherwise, it will have to let its artificially depreciated currency

appreciate. This is interesting and perhaps topic for another future

article.

Negative Feedback Mechanism

Example of negative feedback system

Wikipedia defines negative feedback as following “

Negative

feedback occurs when the result of a process influences the operation of

the process itself in such a way as to reduce changes.” In order

to understand this concept look at the adjacent diagram (Again taken

from Wikipedia). As you can see in the diagram, when water level in the

reservoir decreases, the piston stopping water flow is lifted and water

starts to pour in. When water is filled, the piston will again come down

to stop more water from pouring and this will maintain the water at

desired level. The equilibrium level of water will be determined by the

arrangement of the system rather than the flow of water.

Similar negative feedback system exists in economics. For example,

consider exchange rate and export-import. Actual situation will be very

complicated because of a large number of variable interacting together.

To keep things simple, we will consider only two variables at a time –

export-import and exchange rate. As we have discussed above,

appreciation currency causes increase in import while discourages

export. This will lead to increase in demand for foreign currency and

simultaneously increase in supply of local currency. This putting a

downward pressure on exchange rate. If government does not interfere and

there is no net capital flow, then exchange rate will quickly adjust

such that values of imports and exports are perfectly matched.

Relation between interest rate and exchange rate (Interest Rate Parity)

Another beautiful example of such feedback system is interest rate

parity. In order to explain it lets assume Interest rate for borrowing

in USA is 4% and interest one gets on government bond in India is 8%. It

will make perfect business sense if you borrowed $1000 from USA,

purchased Indian government bond and after a year you got interest of

$80. Paid $40 as interest to the bank you borrowed from, and made a

profit of $40. That without investing a single penny of your own. Such

situation where you can make money without investing any capital at all

is called arbitrage (which in itself is fascinating financial concept

and deserves a complete article on itself).

The only problem with this is it will not be only you who can think

of this. Other people too would want to make profit out of this

opportunity and soon there will be many dollars flowing from USA to

India causing Indian Rupee to appreciate in comparison to USD and

whatever gains you could make from excess interest rate will be offset

by the increase in exchange rate.

Self fulfilling prophecies or Positive Feedback

Directly opposite to the concept of Negative feedback is Self

Fulfilling Prophecies or Positive feedback. For example suppose there is

a rumor, completely unfounded, that the price of gold is going to

increase to very high in a week. People will want to profit from this

information and will buy some gold to sold later at higher price.

Initially, some people will be fooled by the rumor and buy gold. This

temporary surge in short term demand will lead to momentary increase in

price. This increase in price will give credence to the rumor, and more

people will flock in to buy gold. This will further increase the price,

pulling even more people. The rumor, which originated without any

analysis or “fundamental” cause, was the reason itself for the rumor

becoming true.

Such positive feedback are very common in our life, engineering and

economics. In context of exchange rate, sometimes positive feedback

plays a prominent role. Suppose, all the traders in foreign exchange

market believe that rupee has depreciated far below its ‘intrinsic’

value and it will appreciate in near future. In order to profit from

this anticipated gain, they will try to hoard the rupee, thus increasing

its demand and causing it to appreciate.

Opposite of this is also true. If traders believe that rupee (or for

that matter any currency) is about to depreciate, they might actually

trigger it by shorting the currency.

The paradox of negative and positive feedback

What seems to be positive feedback in short term might actually be

negative feedback if looked broadly. For example, lets look at the

currency example again. The general belief that currency has fallen far

below its true value caused it to appreciate through positive feedback

mechanism. But, at the same time it also prevented currency to

depreciate further and hence acted as negative feedback.

Existence of negative and positive feedback loops give rise to

several interesting phenomena in economics and in other areas. But the

article has already surpassed 2600 words, so I can not give many

examples. However, one example very crucial to our ongoing discussion

can not be omitted. It is what economists say

Impossible Trinity.

Impossible Trinity

The concept of impossible trinity states that a country (or an

economy) can not simultaneously have Fixed exchange rate, Free capital

flow and independent monetary policy (which roughly means control over

interest rate).

For example, suppose India pegs its currency to say Rs. 60/$ and

intends to maintain free capital flow. Now, if it sets interest rate

that is higher than that of USA, then money will start flowing in from

US to bank on this arbitrage opportunity (as we discussed earlier). So,

in order to maintain its exchange rate, it will have to buy Dollars. But

it will have a limit to how much it can buy. Similarly, if it sets

interest rates lower than US, money will start flowing out. To prevent

rupee from falling, it will have to sell off its dollar reserve. But

that can last only till its reserves gets fully depleted. Thus

government will have to set interest rate equal to that of US.

If you look closely, India, in recent times, has tried to achieve

this impossible trinity to some extent. It kept currency undervalued,

wanted foreign investors to come in, and had to increase interest rate

to contain inflation. What makes this more ludicrous is that it was

attempted when our premier is a trained economist!

Now let us look at the unprecedented devaluation of rupee more closely.

Causes

What is good for Economy is bad for Politics: India’s trade balance

is highly unfavorable. What this means is India imports far more than it

exports. In fact, Indian export is only about 80% of its imports, a

deficit of about $ 120 bn (2011). This deficit is largely balanced by

remittances (which stood at $69 bn in 2012), FDIs and FIIs.

Economically it makes sense for India to let its currency appreciate

because it will make imports cheaper and help reduce its trade

imbalance. But, appreciating currency will have negative impact on its

exports. Now, India mainly exports labor intensive goods and services –

Software services, polished diamond, textiles, processed cashew nuts,

leather goods. These sectors generate huge employment. Appreciation of

currency causes fall in the profitability in these sectors, leading to

many people loose their jobs. Looked from perspective of politicians,

this is hugely unpopular.

Even though the overall gain from appreciated rupee is far more than

the losses, gains per individual are small in magnitude and distributed

over a large population; whereas losses per individual is large and

concentrated in minority of the population. Such policies are impossible

to pursue in a democracy like India because those at loss will be far

more vocal while people at gain will not bother at all.

Under such political considerations, our government, a coalition of

several parties can not afford to be bold. So, in last 5-6 years, driven

by impressive economic growth of India, when foreign investors flocked,

there was upward pressure on the rupee. Government was unwilling to let

rupee appreciate and kept it artificially devalued. In the process it

amassed huge foreign exchange reserves (about $300bn). Where did the

government bring this money from? It simply printed the money!

Printing of more money causes inflation, another politically

unpopular thing. So, in order to curb the money supply, government

issued bonds under Market Stabilization Scheme (MSS bonds). It did curb

the inflation to some extent, but when bond matures, government has to

pay the money along with the interest. So, this scheme does not really

curb inflation, it postpones it. When those bonds matured, government

made payments, again by printing more money, as government is running

budget deficit and does not have income to pay. This caused inflation

which you might have noticed during recent times. How does government

curb inflation now? It increased interest rate to reduce the supply of

money.

Increase in interest rate caused a slowdown in growth. Also, global

economic slowdown reduced demand for India exports and exports fell too

(about 30% in last year). Import however, did not fall by that amount

because Oil, the major component of our imports, is essential commodity.

So the trade balance turned more unfavorable. Also, looking at the

slowing pace of growth new investor abstained from investing in India

and older investor too started to get uneasy. As they tried to pull back

their money, it put downward pressure on rupee.

If foreign investor expects the currency of a country to fall, it

will withdraw its investments because its investment value will fall

with the currency. For example suppose you invested $1000 at Rs.40/$. So

your investment in India is Rs. 40000. Tomorrow if rupee falls to Rs.

60/$ then value of your investment has fallen to $667. Foreign investors

fearing further fall in rupee started to flee Indian market and this

put further downward pressure on rupee (Positive feedback). Government

could interfere, but owing to its huge budget deficit, had limited

resources and rupee had a free fall. There is more to it, but the

article swelling like Dollar

Impact

Economists do not agree about impact of nominal exchange rate on real

economy. Many argue that Nominal values do not have any impact on real

economy while others claim that the effect nominal variables have on

human psychology and expectations of future does hamper real economy

(applying positive feedback, you can see how?).

Two very visible impacts are 1. increasing oil prices and 2. India

gaining competitive advantage in certain export. Why oil price is

increasing is quite obvious. The later impact needs some elaboration.

What has made the devaluation of rupee more problematic is global

slowdown. Alternatively, it might well be that this downfall was brought

about by the global slowdown. But in either cases, the demand for goods

and services in developed economy is dwindling. But demand in certain

goods like textile will not be impacted that much (people are not going

to shun wearing cloths because of slowdown). Main competitor of India in

such sector is China. During the same period when Indian rupee has been

falling, salaries of labors in China has been on the rise. This had

made Indian export more favorable.

Another impact, which may seem like silver lining in the dark cloud

is that it has forced government to bring certain economic reforms (FDI

in retail and other sectors) and has brought a near crisis like

situation which can force unwilling government to bring reforms (as it

did in 90s).

Remedy

Government has tried several things to control downward spiraling

rupee but those steps are too little, too late and many are pointed in

wrong direction; like curbing import of gold. A government should not be

telling people what to buy and what not to buy. Demand of gold in India

is culture induced. Also, demand of gold increases when economic

uncertainty increases. Trying to micromanage people’s behavior will have

undesirable impact in long term.

There are not many options in short term, but in long term government

needs to bring reforms pending for many decades. Those reforms need

strong political will and I seriously doubt it can be effected without

another crisis. Lets see!

I started out this article in response to questions students have

been asking me about falling rupee. When I set out to explain, it soon

reached epic proportions. I have a lot more to say, but 3800 words are

way too much to read in one sitting. It took me more than a week and 5-6

sessions to write. Will say more later or in comments.